Global Ecommerce Infrastructure Evolves as Major Platforms Integrate Generative Artificial Intelligence and Specialized B2B Management Tools

The digital commerce landscape has entered a period of rapid technological consolidation and expansion, characterized by the integration of sophisticated artificial intelligence and the democratization of enterprise-grade tools for small and medium-sized businesses. This week’s developments across the ecommerce sector reveal a strategic shift toward "agentic commerce," where AI-driven assistants handle complex reporting, and the removal of traditional barriers between direct-to-consumer (DTC) and business-to-business (B2B) operations. From Shopify’s expansion of native wholesale features to the rise of specialized apparel fulfillment and AI-powered business formation, the latest updates signal a maturing industry focused on operational efficiency and cross-channel visibility.

The Democratization of B2B Ecommerce

For years, the ability to manage complex wholesale operations was a luxury reserved for high-revenue enterprises with the budget for custom plugins or expensive platform tiers. This paradigm shifted significantly this week as Shopify announced the extension of its native B2B features to all merchants. Previously restricted to the Shopify Plus tier, foundational B2B tools are now available to users on Basic, Grow, and Advanced plans at no additional cost.

This move addresses a growing trend in the "prosumer" and small business market where brands are increasingly hybrid, selling both to individual consumers and retail partners. The update allows smaller merchants to manage company profiles for wholesale buyers, establish custom catalogs with tailored pricing, and implement volume discounts without the "patchwork" of third-party applications that often slow down site performance. By including features like vaulted credit cards and flexible payment terms, Shopify is effectively lowering the entry barrier for small brands to enter the global wholesale market, which is projected to reach trillions in digital sales by the end of the decade.

Complementing this shift in the enterprise space, Commercetools has partnered with TradeCentric to streamline e-procurement. While Shopify targets the emerging wholesale merchant, the Commercetools-TradeCentric alliance focuses on global enterprises. This partnership integrates Commercetools’ "headless" commerce architecture with TradeCentric’s B2B connected commerce network, which supports over 220 procurement platforms. The goal is to eliminate manual order processing—a notorious source of friction and error in large-scale B2B transactions—and accelerate the order-to-cash cycle.

The Rise of Generative AI in Operational Management

Artificial intelligence is moving beyond simple chatbots and content generation into the realm of "operational intelligence." Miva’s release of its 26 R1 update exemplifies this trend with the introduction of an embedded AI reporting assistant. Dubbed "AI Insights," this tool allows merchants to query their store data using natural language. Instead of building complex Excel dashboards or exporting CSV files, a merchant can simply ask the platform to "identify the top-performing products by category over the last quarter" or "summarize conversion rate fluctuations during the holiday weekend."

This move toward conversational data analysis is mirrored by Bitly, which has launched "Assist" and "Weekly Insights." As the industry’s leading URL shortener and QR code provider, Bitly is leveraging generative AI to help marketers understand the "why" behind their click data. Bitly Assist functions as an AI-powered chat assistant that explains performance trends across different geographies and devices, effectively acting as a junior data analyst for small marketing teams.

Furthermore, the integration of AI into the very foundation of business creation has been realized by Swyft Filings. The company has launched an OpenAI app that allows entrepreneurs to form an LLC or register a corporation directly within the ChatGPT interface. By utilizing generative AI to provide real-time guidance on legal structures and filing requirements, Swyft Filings is shortening the distance between an idea and a legally recognized business entity.

Specialized Logistics and the Apparel Sector

As the general ecommerce market becomes more crowded, logistics providers are turning toward specialization to provide value. ShipMonk, a global leader in fulfillment, has opened a new 406,000-square-foot facility in Louisville, Kentucky, designed specifically for the unique demands of apparel brands.

The apparel industry faces specific challenges, including high SKU counts due to size and color variations, as well as high return rates. ShipMonk’s new facility addresses these through high-density storage layouts and dedicated "rework stations" for handling returns and refurbishments. Additionally, the facility offers on-site embroidery services, allowing brands to offer premium customization without adding another leg to the supply chain. The choice of Louisville is strategic, as it sits near major shipping hubs, including the UPS Worldport, ensuring that apparel brands can meet the increasingly tight delivery windows demanded by modern consumers.

Amazon Ecosystem: Transparency and Advertising Optimization

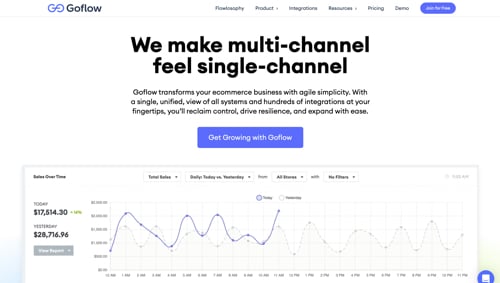

The Amazon marketplace continues to be the primary theater of competition for many third-party sellers, leading to a surge in tools designed to manage the platform’s increasing complexity. Goflow has introduced an "Order-Level P&L" feature to provide real-time profit tracking. For Amazon-first merchants, understanding true margins is often difficult due to fluctuating shipping rates, storage fees, and inventory costs. Goflow’s new tool estimates margins by pulling data from inventory batch costs and shipping inputs, providing transparency at the SKU and channel level.

In the realm of advertising, BQool has released an AI-powered solution for Amazon sellers to automate campaign management. The system features "auto-harvesting," which identifies high-performing keywords from search term reports and automatically integrates them into active campaigns. This level of automation is becoming a necessity as Amazon’s advertising environment becomes more "pay-to-play," requiring constant optimization that manual management can rarely achieve.

Additionally, Levanta’s acquisition of Perch+ signals consolidation in the affiliate marketing space for Amazon. By bringing Perch+ into its ecosystem, Levanta allows brands to work directly with 60,000 partners while utilizing Amazon Attribution to track exactly which creators are driving sales. This provides a level of data granularity that was previously difficult to achieve in influencer marketing campaigns.

Enhancing Visibility in the Age of AI Search

Perhaps the most forward-looking update comes from Durable, which has launched "Discoverability." As consumers move away from traditional search engines like Google and toward generative AI platforms like ChatGPT, Gemini, and Perplexity, businesses face a new challenge: how to be "found" by an LLM (Large Language Model).

Durable’s new tool provides a metric for how findable a business is across these AI channels and offers suggestions for improving what is becoming known as "Generative Engine Optimization" (GEO). This represents a fundamental shift in digital marketing strategy, moving from keyword-stuffing for Google to structured data and brand authority for AI training sets.

Connectivity and Payment Infrastructure

The technical "plumbing" of ecommerce also saw significant upgrades this week. SDLC Corp launched a free connector for Odoo and WooCommerce, bridging the gap between one of the world’s most popular storefronts and a powerful open-source ERP (Enterprise Resource Planning) system. This connector uses webhook-based processing to ensure that inventory and catalog data remain synchronized in real-time, a critical requirement for multi-store environments.

On the financial side, BitRail has partnered with Payment Lock to launch a merchant payment suite focused on fee reduction. By offering branded digital wallets and infrastructure that supports compliant pricing for both cash and credit, BitRail is helping merchants reclaim margins lost to traditional credit card processing fees.

Finally, Criteo has expanded its "Go" self-service advertising platform to include small and midsize businesses. By unifying display, video, and social advertising into a single environment powered by generative AI creative tools, Criteo is allowing SMBs to run sophisticated retargeting campaigns that were once the exclusive domain of major retailers with massive ad budgets.

Broader Impact and Industry Implications

The collective weight of these updates suggests a significant transition in the ecommerce industry. We are moving away from a period where merchants had to be "integrators"—spending their time connecting disparate tools—toward a period where platforms are "intelligent ecosystems."

The focus has shifted from mere transaction processing to comprehensive business management. Whether it is Shopify making B2B accessible to the masses or Miva making data analysis as simple as a conversation, the goal is to reduce the "cognitive load" on the merchant. For the small business owner, these tools provide a competitive edge, allowing them to operate with the sophistication of a much larger corporation. For the consumer, these backend efficiencies typically translate to more personalized shopping experiences, faster delivery, and more diverse product availability across multiple channels.

As we look toward the second half of the year, the successful implementation of these AI and B2B tools will likely define the winners and losers in an increasingly automated and integrated global marketplace.

{kind=link}