Okta’s Remarkable Financial Turnaround Driven by Strategic Go-to-Market Revamp Under CRO Jon Addison

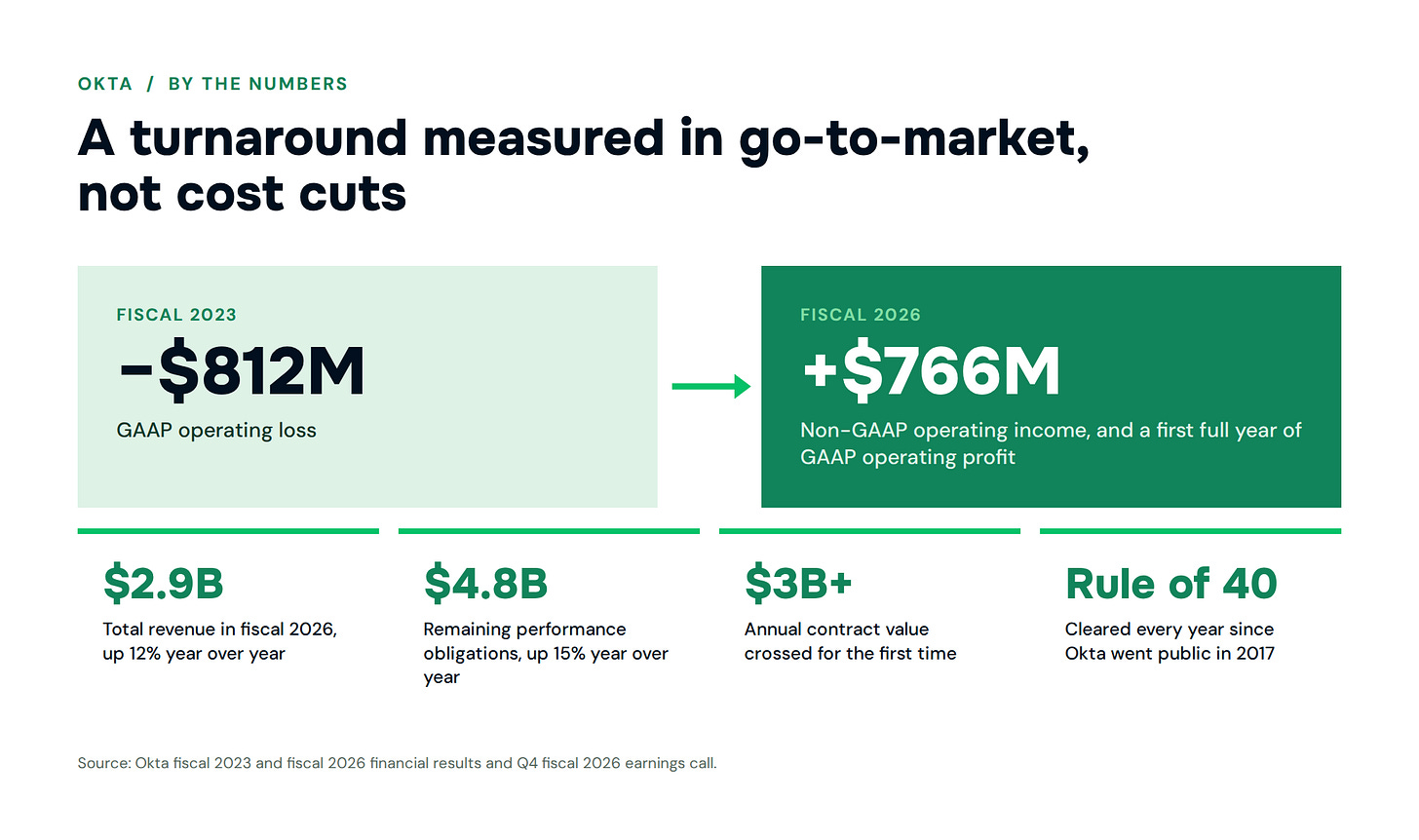

Okta, a leading identity and access management provider, has orchestrated an impressive financial turnaround, transitioning from a significant operating loss in fiscal 2023 to robust profitability by fiscal 2026. This transformation, largely attributed to a series of strategic Go-to-Market (GTM) initiatives spearheaded by Chief Revenue Officer Jon Addison, offers critical insights for B2B software and AI leaders navigating dynamic market landscapes. The company reported an operating loss of $812 million in fiscal 2023 but concluded fiscal 2026 with $766 million in non-GAAP operating income, marking its first full year of GAAP operating profit, alongside a substantial $252 million in free cash flow in the final quarter alone. While cost-cutting measures played a role, the core of Okta’s resurgence lies in a meticulously redesigned GTM strategy, focusing on specialization, partner-led growth, an evolved sales methodology, and a keen understanding of the AI adoption cycle.

Navigating Turbulence: Okta’s Journey to Profitability

Okta’s dramatic financial pivot comes after a challenging period. Fiscal 2023 saw the company grappling with an $812 million operating loss, exacerbated by both internal and external pressures. Internally, Okta was absorbing the fallout from a series of security breaches, most notably an October 2022 incident involving a third-party vendor and a subsequent January 2023 breach impacting its customer support systems. These events, while common in the cybersecurity industry, tested customer trust and necessitated significant investment in remediation and enhanced security protocols. Externally, the broader technology market had shifted its focus from "growth at any cost" to profitability and efficiency, making investor sentiment particularly sensitive to financial performance.

It was against this backdrop that Jon Addison stepped into the role of interim Chief Revenue Officer in February 2023, taking the position permanently in November of the same year. His mandate was clear: to stabilize the company and steer it towards sustainable growth and profitability. The conventional wisdom for turnarounds often defaults to aggressive cost reduction. While Okta did implement spending controls, the more impactful and strategic changes originated from Addison’s comprehensive re-evaluation and overhaul of the company’s GTM engine. His approach prioritized revenue generation and market penetration through structural and methodological innovations, proving that a strong GTM can be the most potent lever for financial recovery and sustained success.

The Go-to-Market Playbook: Four Pillars of Okta’s Resurgence

Addison’s playbook, distilled from his extensive experience across prior platform shifts like the internet and cloud, identifies four key GTM lessons critical for B2B software and AI companies. These lessons are not merely tactical adjustments but fundamental shifts in how Okta engages with its market, sells its diverse product portfolio, and builds lasting customer relationships.

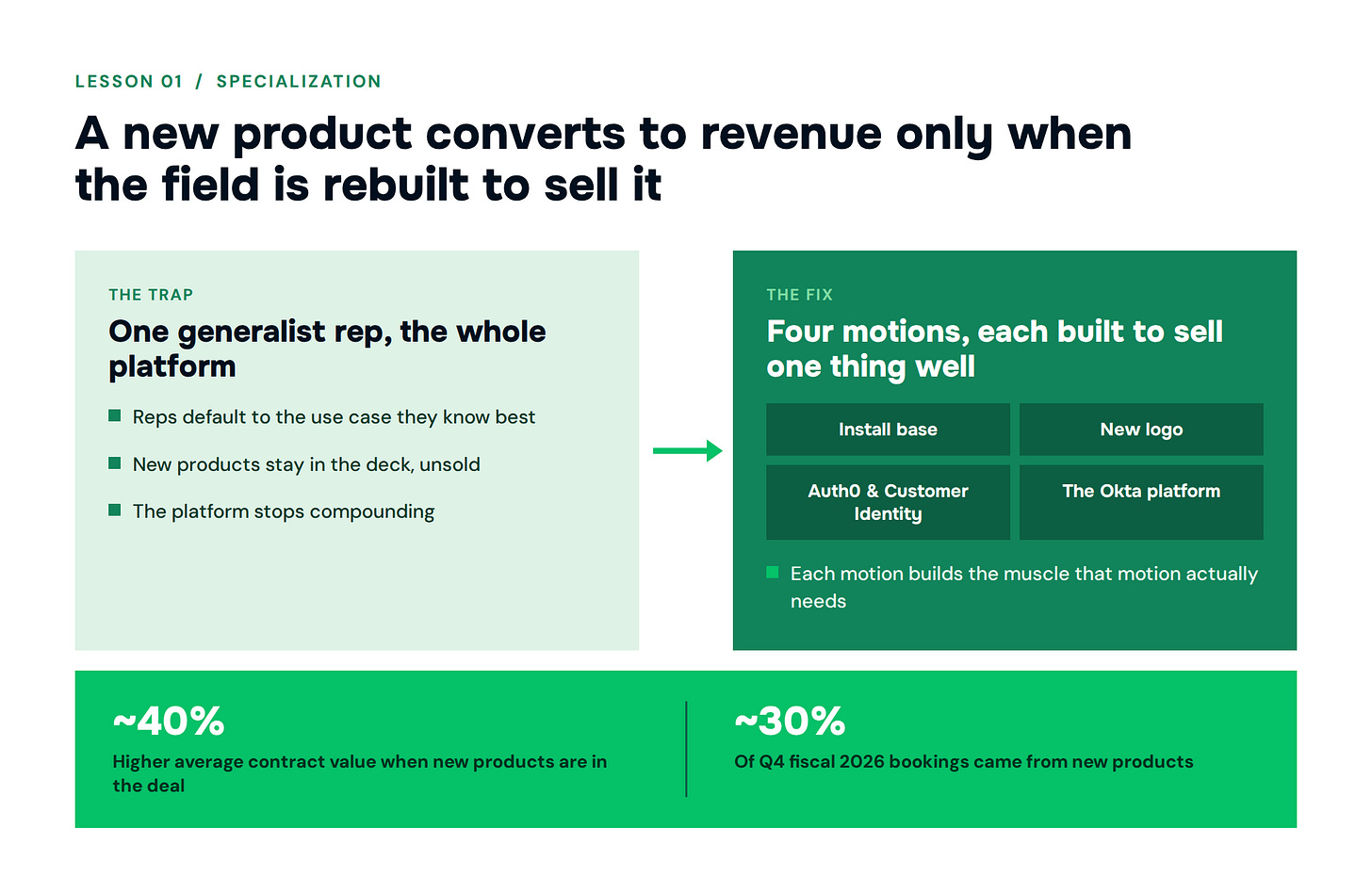

1. Specialization as the Catalyst for Platform Breadth

Okta’s product portfolio is vast, encompassing workforce identity, customer identity (via Auth0), privileged access, identity governance, and an emerging suite for securing AI agents. While this breadth is a significant competitive asset, it can also become a sales impediment if not managed correctly. The "generalist rep trap" is a common industry challenge: when tasked with selling a wide array of products, sales representatives often gravitate towards the one they understand best, neglecting newer or more complex offerings. This stifles the growth of emerging products and prevents the platform from realizing its full compounding potential.

Jon Addison’s solution was a structural reorganization of Okta’s field sales teams around specialization. Instead of a single generalist motion, Okta implemented distinct sales motions tailored for different segments: the existing install base, new logo acquisition, Auth0 and customer identity solutions, and the broader Okta platform offerings. This specialization allows each team to develop deep expertise in specific product areas and customer needs, building the "muscle" required to effectively articulate value and close deals for even the most nascent modules.

The impact of this reorganization has been significant. During Okta’s Q4 fiscal 2026 earnings call, CEO Todd McKinnon highlighted that new products, including Identity Governance, Privileged Access, and the recently launched AI agent security solutions, accounted for approximately 30% of total bookings in the quarter. Furthermore, deals that included these new products demonstrated an average contract value (ACV) that was about 40% higher than deals without them. Okta Identity Governance, for example, has garnered over 2,000 customers in just over three years since its launch, a testament to the effectiveness of a specialized sales approach.

This strategy mirrors lessons learned by other enterprise software giants. Salesforce, over a decade, discovered that multi-product expansion and industry-specific clouds only truly pay off when the sales force is organized to sell them effectively, leading to their implementation of specialist overlay teams and industry-focused sales. Similarly, Rippling, designed as a compound product from its inception, employs distinct sales motions for each module. The overarching implication for the B2B sector is clear: simply developing more products is insufficient; the Go-to-Market organization must be redesigned to actively sell them, ensuring that product innovation translates directly into increased average contract value and market penetration. An organization that observes its reps consistently selling only a subset of available products despite a broad portfolio has an organizational design gap that demands attention.

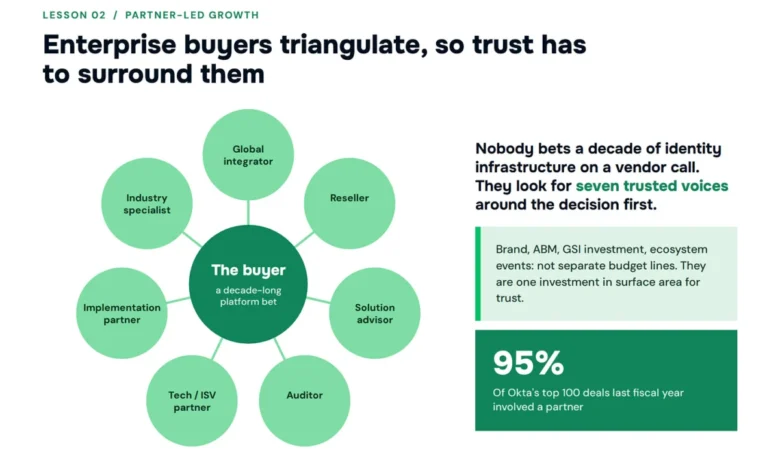

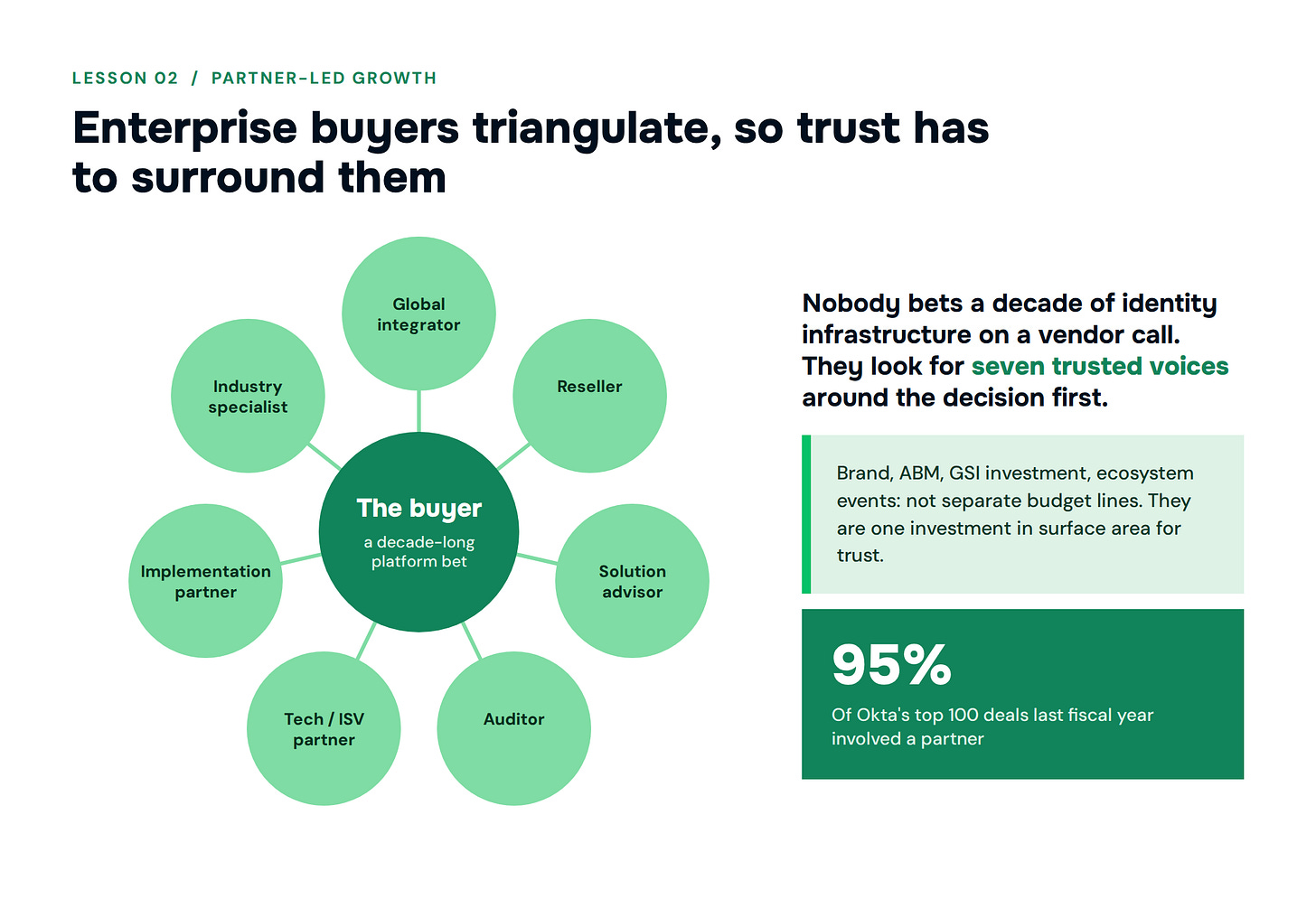

2. Partner-Led Growth: A Three-Year Cultural Rebuild, Not a Program

A crucial element of Okta’s GTM transformation is its profound commitment to partner-led growth. In the last fiscal year, an astounding 95% of Okta’s top 100 deals involved a partner. However, Addison cautions against viewing this achievement as the result of a simple "program." He emphasizes that building such a robust partner ecosystem is a multi-year cultural rebuild, demanding consistent strategic direction, meticulous incentive alignment, proactive friction removal, and substantial investment in what he terms "partner practices."

The distinction between a "partner program" and a "partner practice" is fundamental. A program often implies a transactional relationship, offering a portal and a margin table. A practice, conversely, signifies a deep, symbiotic relationship where partners become genuine experts in the customer’s business, while Okta remains the expert in identity. This allows for a more holistic, trusted advisory role for the partner, which is invaluable in complex enterprise sales, particularly in cybersecurity.

Addison articulates the underlying math of this strategy: in enterprise cybersecurity, where companies make generational, multi-year platform bets, a decision is rarely made based on a single vendor call. Instead, buyers seek corroboration and validation from multiple trusted sources. "We need seven partners to surround that customer who also trusts us," states Jon Addison. This perspective redefines the allocation of marketing and sales resources. Initiatives like F1 sponsorships, account-based marketing, investments in global system integrators, brand campaigns, and ecosystem events are no longer viewed as disparate budget lines but as integrated components of a broader strategy to build a "surface area for trust to accumulate around the buyer."

This approach is not unique to Okta but is a proven model in the cybersecurity space. Industry leaders like CrowdStrike and Palo Alto Networks have built significant portions of their enterprise distribution through extensive channel partners and global system integrators. Security leaders, when committing to a platform for the next decade, inherently seek independent validation before signing a deal. Many companies tend to treat partners as an auxiliary distribution channel. Okta, however, has integrated partners as a core growth engine, building its entire GTM organization around this conviction. This long-term commitment explains why Addison views their partner ecosystem as still being in its early stages, despite three years of intensive development.

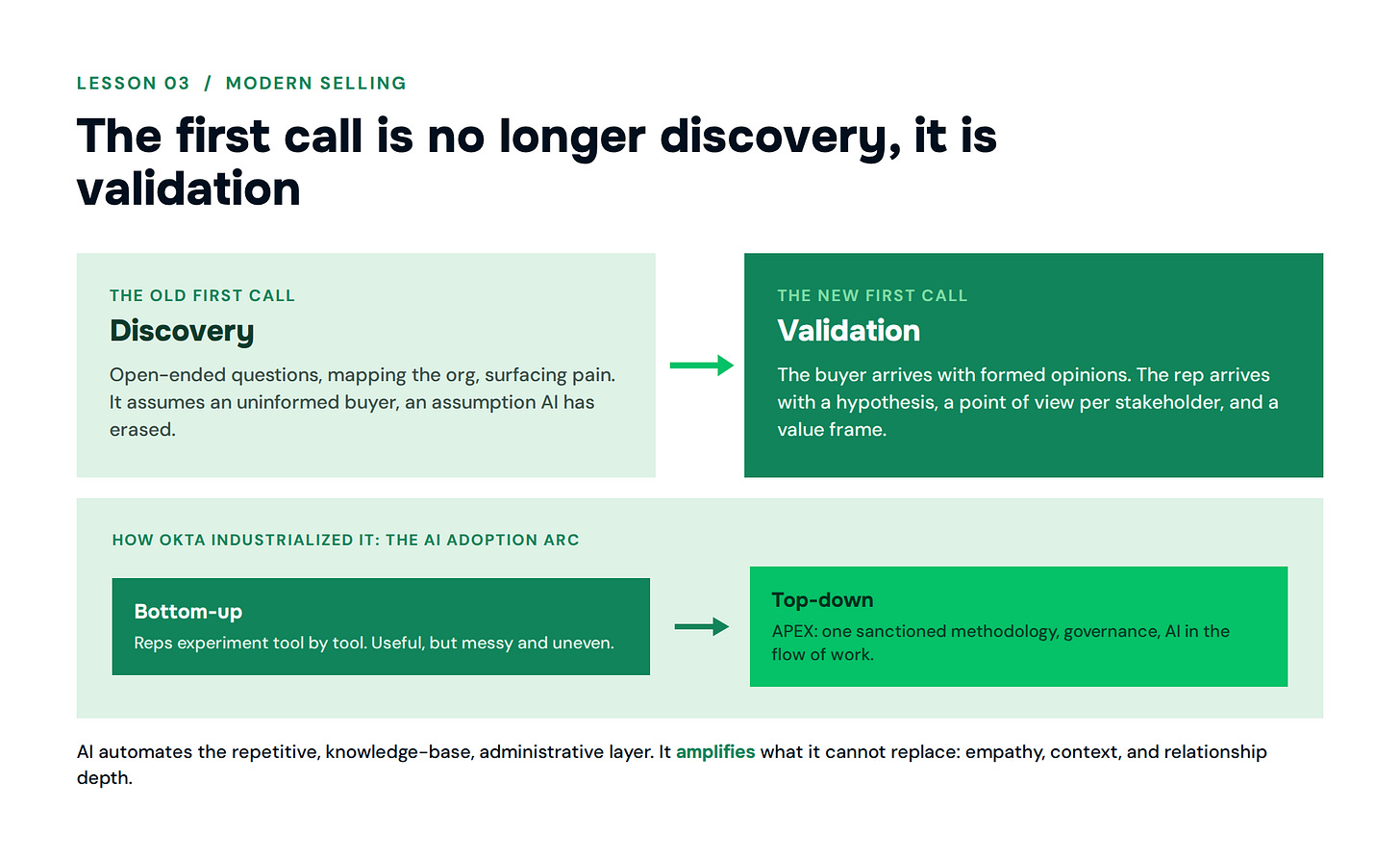

3. The Evolving Sales Cycle: From Discovery to Validation

The nature of the B2B sales process has fundamentally changed in the digital age. Buyers are no longer passive recipients of information during an initial "discovery call." Instead, they arrive at the first interaction armed with extensive research, strong pre-formed opinions about products, competitors, and potential solutions. Jon Addison’s reframe of the salesperson’s role is particularly incisive: "The first call is no longer discovery. It’s validation."

This shift means that a generic discovery deck is now a fast track to losing a deal. The successful sales representative must arrive with a well-developed hypothesis about the buyer’s needs and how their product can specifically address them, ready to either validate or subtly correct the buyer’s existing beliefs. This perspective is echoed by industry experts like Sam Senior, CEO of TestBox, who notes that 70-80% of the B2B purchase decision now occurs before the first sales call, and vendor shortlists have shrunk to one or two names. The sales rep’s primary objective on that crucial first call is to confirm or refine what the buyer already thinks they know.

Okta’s internal response to this evolution is a new sales methodology called APEX, built upon the "Command of the Message" framework and specifically recalibrated for the AI era. This methodology equips reps with value frameworks tailored to each new product, differentiated points of view for various stakeholders involved in a deal, and, critically, embeds AI tools directly into the sales workflow. These AI tools include conversational intelligence for real-time insights, quoting agents for efficient proposal generation, and pre-sales assistants to augment preparation.

Initially, Okta’s AI adoption within the sales field was a bottom-up, experimental process, with reps independently exploring various tools. While yielding some benefits, it also created a degree of disorganization. The shift in the current year has been a top-down industrialization of this experimentation, establishing a sanctioned methodology, setting clear governance, and making deliberate bets on scalable AI tools. This transition from individual tinkering to a unified, AI-enhanced methodology is where significant productivity gains compound. This redefined sales approach emphasizes that repetitive, knowledge-based administrative tasks are automated by AI, allowing human sales professionals to amplify their uniquely human skills: empathy, nuanced contextual awareness, and the ability to build deep, trust-based relationships.

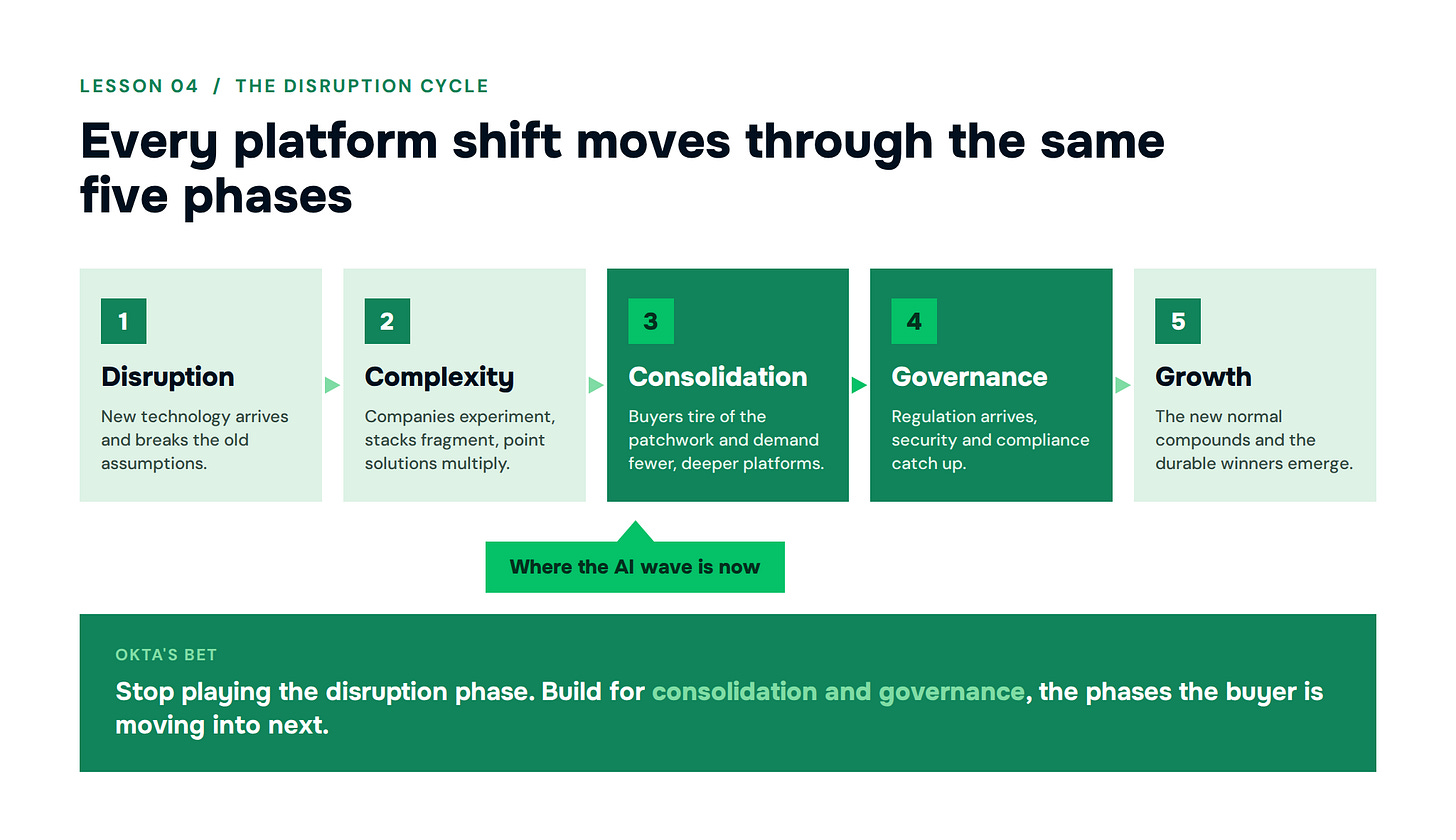

4. Aligning GTM with the AI Disruption Cycle

Drawing from his experience across previous platform shifts (the internet and the cloud), Jon Addison frames the current AI wave through a five-phase disruption cycle:

- Disruption: New technology emerges, breaking old assumptions.

- Complexity: Companies experiment, leading to fragmented stacks and point solutions.

- Consolidation: Buyers tire of patchwork solutions and demand fewer, deeper platforms.

- Governance: Regulators catch up, and security and compliance become paramount.

- Growth: The new normal compounds, and durable winners emerge.

Addison asserts that the AI wave is still experiencing "a significant amount of disruption." However, Okta’s strategic logic positions the company not in the crowded "disruption" phase, but squarely in the consolidation and governance phases. Okta aims to be the neutral, independent platform offering complete identity coverage for all entity types—human, machine, and critically, AI agents—designed to absorb complexity rather than create it.

Okta’s internal research underscores this strategic focus: 91% of organizations are already deploying AI agents, yet only about 10% have a developed strategy for managing these non-human identities. This significant gap represents the core consolidation and governance opportunity that Okta is actively targeting. The company recently launched "Okta for AI Agents" with general availability on April 30, 2026. Furthermore, its "Cross-App Access" standard, designed to govern how AI agents connect across various applications, has been integrated into the Model Context Protocol, indicating a proactive approach to industry standards.

All of Okta’s GTM initiatives—the partner ecosystem rebuild, the platform specialization, the focus on AI governance products, and the APEX sales methodology—cohere around this central thesis. As the AI wave inevitably shifts from initial deployment to the imperative of managing and securing these agents, Okta aims to be the comprehensive, consolidated answer that buyers will seek. This pattern has historical precedent: the marketing technology landscape in the 2010s saw an explosion of point solutions before buyer fatigue drove consolidation onto a handful of integrated suites. Similarly, the security industry is currently undergoing a mid-consolidation phase, with players like Palo Alto Networks actively pushing customers towards platform adoption over fragmented best-of-breed solutions. The companies that ultimately win the consolidation phase are often not the initial disruptors, but those that anticipate the cycle’s progression and build their GTM for the phase the buyer is about to enter.

Broader Industry Trends and Insights from the GTMnow Network

Beyond Okta’s specific strategies, the broader B2B software and AI landscape continues to evolve at a rapid pace, as highlighted by recent developments shared within the GTMnow network.

CRM Evolution: AI Agents as Infrastructure: A recent a16z piece provocatively suggests that AI agents are transforming Customer Relationship Management (CRM) platforms in a way analogous to how newsfeeds reshaped social graphs. This implies that CRMs, traditionally central systems of record, are becoming more foundational infrastructure, with AI agents taking on a more active, dynamic role in driving customer interactions and automating workflows. This shift will likely necessitate CRMs to be more open, extensible, and AI-native, focusing on enabling intelligent automation rather than merely storing data.

CNBC Disruptor 50: AI Dominance: The 2026 CNBC Disruptor 50 list showcases the pervasive influence of Artificial Intelligence. Anthropic, a prominent AI research and development company, claimed the top spot. A striking 43 out of the 50 recognized companies cited AI as essential to their core business model, reflecting AI’s fundamental role in driving innovation and disruption across industries. The total implied valuation of these companies tripled to $2.4 trillion, underscoring the immense capital flowing into AI-driven ventures. Notably, GTMfund portfolio companies like Vanta and Armada were also recognized on this prestigious list, highlighting their impactful contributions to the evolving tech landscape.

Key Talent Movements in AI: The talent war in AI remains fierce. Andrej Karpathy, a co-founder of OpenAI and a highly respected figure in the AI community, recently joined Anthropic’s pre-training team. His move signals Anthropic’s aggressive pursuit of top-tier talent and its commitment to accelerating pre-training research, leveraging Claude’s capabilities to push the boundaries of AI development. Such high-profile talent shifts often indicate significant strategic plays within the competitive AI ecosystem.

Strategic Acquisitions and Growth in B2B Tech: The B2B sector continues to see strategic consolidation and growth. Sendoso, a leading gifting platform, acquired Merch.co, marking its third acquisition in two years. This move positions Sendoso as the only end-to-end gifting platform, offering a comprehensive solution from ideation to delivery. This acquisition strategy highlights the drive for integrated solutions and expanded market reach within niche B2B service areas.

Major Funding Rounds: Powering the Next Wave: Significant funding rounds continue to fuel innovation across the B2B and AI sectors.

- Mercury: The financial OS for startups raised $200 million at a $5.2 billion valuation, reporting four consecutive years of growth and profitability. Serving over a third of U.S. startups, Mercury’s acquisition of an AI-native payroll solution and conditional bank approval positions it to become the comprehensive financial backbone for the next generation of builders.

- Exa: Focused on building the "search engine for AI," Exa secured $250 million at a $2.2 billion valuation. Its API is already utilized by over 5,000 companies and 400,000 developers, including major players like Cursor, Cognition, and HubSpot. This substantial investment underscores the critical need for advanced search and data retrieval capabilities to power increasingly sophisticated AI applications.

- Armada: A GTMfund portfolio company, Armada raised a $230 million Series B and launched Galleon Forge One, a facility dedicated to manufacturing and deploying modular data centers globally. This initiative addresses the growing strategic priority of infrastructure sovereignty as the AI race accelerates, providing the industrial base for distributed AI compute.

- Polsia: This company, achieving nearly $10 million ARR with just its founder, raised $30 million at a $250 million valuation. Polsia focuses on the orchestration of AI agents to perform core business functions like coding, research, cold outreach, paid ads, and support, tackling the "unglamorous middle" of business operations. This signals a growing market for AI solutions that automate and optimize operational workflows.

- Pivot: Securing $40 million in Series B funding, Pivot aims to replace legacy procurement systems with an agentic AI operating system. Already operating in over 25 countries and processing $3 billion in invoices annually for clients like DoorDash and Lemonade, Pivot exemplifies the AI-driven transformation of traditional enterprise functions, rebuilding them from the system of record upwards.

Conclusion and Outlook

Okta’s journey from a substantial operating loss to robust profitability is a compelling case study in strategic Go-to-Market leadership. Jon Addison’s emphasis on specialization, deeply integrated partner ecosystems, an adaptive sales methodology, and a forward-looking understanding of the AI disruption cycle provides a powerful blueprint for B2B software and AI companies seeking sustainable growth in a rapidly evolving market. The company’s success demonstrates that in an era of increasing complexity and AI-driven transformation, a well-executed GTM strategy, rather than just cost containment, is the ultimate driver of financial health and competitive advantage. As the broader B2B and AI sectors continue their explosive growth and evolution, the lessons from Okta’s turnaround, alongside the innovative strides of other market players, offer invaluable guidance for navigating the opportunities and challenges ahead.

{kind=link}