Strategic Internal Audits: A Comprehensive Guide to Enhancing Business Compliance and Financial Integrity

A nerve-wracking visit from the Internal Revenue Service (IRS) isn’t the sole encounter a business might have with an audit. Far from being a dreaded obligation, audits encompass a broad spectrum of systematic reviews that, when proactively conducted, serve as indispensable tools for maintaining operational excellence, ensuring regulatory compliance, and safeguarding financial health. Understanding how to conduct these vital assessments is paramount for any organization aiming for sustained success and resilience in an increasingly complex economic landscape.

The Foundation: Demystifying the Business Audit

At its core, a business audit is a systematic and independent examination of a company’s financial records, operations, and internal controls to verify accuracy, completeness, and adherence to established policies, procedures, and legal requirements. This rigorous process typically involves a detailed review of transactions, reconciliation of financial statements with underlying books and records, and an evaluation of the systems designed to capture and report financial data.

The primary objective of an audit extends beyond mere number-checking; it seeks to provide assurance to stakeholders regarding the reliability of financial reporting and the effectiveness of operational processes. While the IRS represents a regulatory body that may initiate an external audit, numerous other entities, both internal and external, play a crucial role in the auditing ecosystem. These can include internal audit departments, independent Certified Public Accountants (CPAs), state tax authorities, industry regulators, and even prospective investors or lenders.

Historically, auditing practices have evolved significantly. Tracing back to ancient civilizations where scribes would verify inventories and tax collections, the modern audit gained prominence with the rise of complex corporations and public markets in the 19th and 20th centuries. Landmark legislation, such as the Sarbanes-Oxley Act of 2002 in the United States, further solidified the importance of robust internal controls and independent financial audits following major accounting scandals. This evolution underscores a continuous societal demand for transparency, accountability, and trust in financial information.

While the prospect of an IRS audit can understandably induce apprehension, viewing all audits through this lens can lead to missed opportunities. Regular, proactive audits—particularly those initiated internally—are not merely defensive measures. They are strategic investments that enable businesses to get their financial house in order, identify potential weaknesses, and correct errors before they escalate into costly problems or attract unwanted external scrutiny. For instance, a CPA performing an annual review can uncover discrepancies that, if left unaddressed, might trigger an IRS inquiry. A recent study by the Association of Certified Fraud Examiners (ACFE) highlighted that organizations with strong internal controls experience significantly lower fraud losses and detect fraud more quickly, often through audit mechanisms.

A Spectrum of Scrutiny: Understanding Diverse Audit Types

The nature and scope of an audit are largely determined by its objective and the party conducting it. This diversity necessitates a clear understanding of the various types of business audits that can occur, each serving a distinct purpose:

- Internal Audit: Conducted by employees within the organization, often by a dedicated internal audit department. Its primary focus is on evaluating the effectiveness of internal controls, risk management, and governance processes to improve operational efficiency and ensure compliance with internal policies and external regulations.

- External (Financial) Audit: Performed by independent third-party CPAs or accounting firms. The main goal is to provide an objective opinion on whether the company’s financial statements are presented fairly, in all material respects, in accordance with an applicable financial reporting framework (e.g., Generally Accepted Accounting Principles – GAAP).

- Operational Audit: A systematic review of an organization’s operations to assess efficiency, effectiveness, and economy. It examines the processes and procedures used to achieve business objectives, identifying areas for improvement in resource utilization and performance.

- Compliance Audit: Focuses on determining whether an organization is adhering to specific laws, regulations, policies, or procedures. This can include environmental regulations, labor laws, industry standards, or internal company policies.

- IT Audit: Examines the information technology infrastructure, applications, and processes to assess their reliability, security, and integrity. This audit type is crucial in today’s digital landscape for protecting data and ensuring system functionality.

- Payroll Audit: Specifically reviews payroll records, calculations, tax withholdings, and compliance with labor laws to ensure accuracy and adherence to regulations. This is particularly important given the complexity of payroll taxes and employee compensation.

- Forensic Audit: Conducted when there is suspicion of fraud or financial misconduct. It involves a detailed investigation of financial records to uncover evidence that could be used in legal proceedings.

- Environmental Audit: Assesses an organization’s environmental performance and compliance with environmental regulations.

- Tax Audit: An examination of an individual or company’s tax returns by a tax authority (like the IRS) to verify the accuracy of reported income, deductions, and credits.

While a business will inevitably face external audits from tax authorities or independent financial auditors, the types of audits a company can—and should—regularly conduct internally are primarily those focused on operational improvement and proactive risk management, such as internal audits, operational audits, and payroll audits. These self-initiated reviews are powerful mechanisms for self-correction and continuous improvement.

The Indispensable Value Proposition: Why Audits Matter Beyond Compliance

The notion that conducting an audit is an overwhelming, lengthy, and resource-intensive process often deters businesses. Indeed, a comprehensive audit can span several weeks or even months for larger organizations. However, framing audits merely as burdens overlooks their profound strategic value. Regular audits are not just a "nice-to-have"; they are fundamental to the robust health and long-term viability of any enterprise.

The strategic importance of conducting audits, especially internal ones, is multifaceted:

- Catching Common Accounting Mistakes: Internal audits are an invaluable first line of defense against errors ranging from simple data entry discrepancies to more complex errors of omission or misapplication of accounting principles. By identifying and rectifying these early, businesses prevent them from compounding, which can lead to significant financial restatements, penalties, or even reputational damage.

- Preventing Fraud: A well-structured internal audit program acts as a deterrent to fraudulent activities. By scrutinizing transactions, reconciling accounts, and evaluating internal controls, auditors can uncover red flags and weaknesses that fraudsters exploit. According to ACFE reports, organizations with anti-fraud controls, often bolstered by internal audit functions, experience 50% lower fraud losses.

- Promoting Accuracy in Financial Reporting: Consistent auditing instills a culture of accuracy and attention to detail throughout the financial reporting process. This leads to more reliable financial statements, which are critical for management decision-making, investor confidence, and regulatory compliance.

- Ensuring Regulatory Compliance: The regulatory landscape is constantly evolving. Audits help businesses stay abreast of changes in tax laws, labor regulations, industry-specific compliance requirements, and data privacy mandates. Non-compliance can result in hefty fines, legal battles, and severe reputational harm.

- Improving Operational Efficiency: Beyond financial checks, operational audits analyze business processes to identify bottlenecks, redundancies, and inefficiencies. By streamlining workflows and optimizing resource allocation, audits contribute directly to cost savings and improved productivity.

- Informing Strategic Decision-Making: Accurate and reliable financial data, validated through audits, forms the bedrock of sound strategic planning. Management can make more informed decisions regarding investments, expansion, cost management, and market positioning when confident in the underlying financial intelligence.

- Building Stakeholder Trust: Transparency and accountability fostered by regular audits enhance trust among investors, creditors, customers, and employees. This trust is a valuable intangible asset that can positively influence market perception, access to capital, and talent acquisition.

- Preparing for External Audits: Perhaps one of the most practical benefits is the preparation for inevitable external audits. By conducting internal reviews, a business can proactively identify and resolve issues, ensuring that records are organized, complete, and accurate, thereby streamlining the external audit process and minimizing potential findings.

The good news is that the effort invested in audits yields cumulative benefits. The more organized a business’s records are, and the more frequently audits are conducted, the less time and resources each subsequent audit tends to require. This efficiency gain transforms what might initially seem like an arduous task into a manageable and routine component of sound business management.

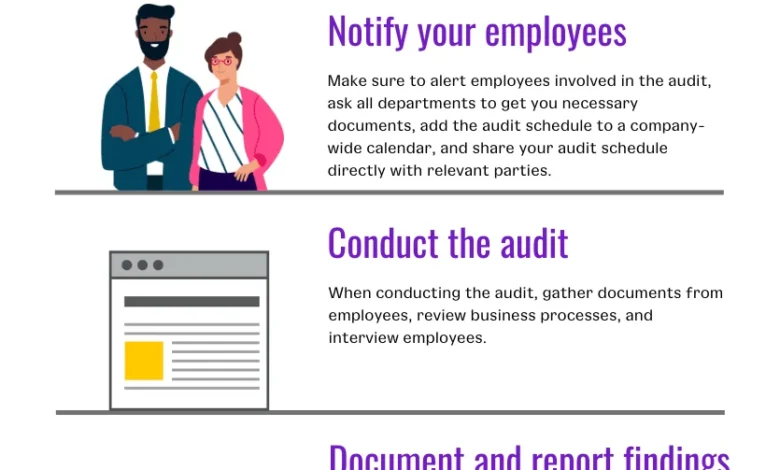

Navigating the Internal Audit Process: A Step-by-Step Guide

To truly reap the benefits of auditing, businesses must adopt a structured approach. While the specific details may vary depending on the audit’s scope, the following five basic steps outline a general internal audit process:

-

Planning and Scoping:

- Define Objectives: Clearly articulate what the audit aims to achieve (e.g., verify payroll accuracy, assess inventory controls, ensure data security compliance).

- Identify Scope: Determine which departments, processes, time periods, and systems will be covered. This involves understanding the business context, potential risks, and areas of concern.

- Resource Allocation: Assign an audit team (internal staff not involved in the day-to-day operations of the audited area, or an external consultant for objectivity), establish a timeline, and allocate necessary resources.

- Risk Assessment: Prioritize audit areas based on identified risks. High-risk areas (e.g., cash handling, complex tax calculations, new system implementations) should receive greater attention.

- Develop an Audit Program: Create a detailed plan outlining specific procedures, tests, and documentation requirements.

-

Fieldwork and Data Collection:

- Information Gathering: Collect relevant documents, records, reports, and data. This includes financial statements, ledgers, invoices, contracts, policies, and procedural manuals.

- Interviews and Observations: Conduct interviews with personnel involved in the audited processes to understand workflows, controls, and potential pain points. Observe operations firsthand to corroborate documented procedures.

- Testing and Analysis: Perform detailed tests on samples of transactions and data. This could involve recalculations, reconciliations, confirmations with third parties, and analytical procedures to identify anomalies or deviations.

- Document Findings: Meticulously record all evidence, observations, and preliminary findings. Ensure that documentation is clear, concise, and sufficiently detailed to support conclusions.

-

Reporting and Communication:

- Draft Audit Report: Prepare a comprehensive report summarizing the audit’s objectives, scope, methodology, findings, and conclusions. Findings should be factual, supported by evidence, and clearly explain the impact or risk.

- Identify Recommendations: Propose actionable recommendations to address identified weaknesses, improve controls, enhance efficiency, or ensure compliance. Recommendations should be practical and measurable.

- Management Review: Share the draft report with relevant management for their review and input. This collaborative step helps ensure accuracy and fosters buy-in for corrective actions.

- Final Report Issuance: Issue the final audit report to appropriate stakeholders, typically including senior management and the board of directors or audit committee.

-

Follow-up and Monitoring:

- Action Plan Development: Work with management to develop specific action plans for implementing the agreed-upon recommendations. These plans should include assigned responsibilities and deadlines.

- Verification of Implementation: Periodically follow up to verify that corrective actions have been implemented effectively and are achieving the desired outcomes. This might involve reviewing updated policies, re-testing controls, or observing new procedures.

- Continuous Improvement: Use the audit findings and follow-up results to refine future audit plans and continuously improve the organization’s control environment and operational processes.

-

Continuous Audit/Monitoring (for mature systems):

- With advancements in technology, some organizations implement continuous auditing, where automated tools monitor controls and transactions in real-time or near real-time, flagging exceptions for immediate review. This proactive approach significantly enhances risk detection and mitigation.

Spotlight on Payroll: Ensuring Accuracy and Compliance

Payroll is a high-risk area due to its complexity, the volume of transactions, and the stringent regulatory requirements from federal, state, and local agencies. A dedicated payroll audit is crucial for maintaining compliance, preventing errors, and avoiding penalties. Preparing for a payroll audit, whether internal or external, hinges on completeness, organization, and diligent reconciliation.

Here’s a detailed, step-by-step approach to preparing for a payroll audit:

-

Systematic Review of Payroll Data and Processes:

- Document Payroll Cycle: Map out the entire payroll process, from time tracking to direct deposit. This includes understanding who is involved, what systems are used, and the internal controls in place.

- Review Employee Records: Ensure all employee master data (names, addresses, Social Security numbers, dates of hire, termination dates, pay rates, deductions, benefit elections) are accurate and up-to-date. Verify I-9 forms for employment eligibility.

- Scrutinize Timekeeping Records: If applicable, review timesheets, time clock reports, or other attendance records for accuracy, proper authorization, and compliance with wage and hour laws (e.g., break times, overtime calculations).

- Verify Wage and Hour Compliance: Confirm that minimum wage, overtime, and meal/rest break rules are being followed according to federal (FLSA) and state laws.

- Examine Deduction and Garnishments: Ensure all deductions (taxes, benefits, 401k, garnishments, child support) are correctly calculated, authorized, and remitted to the appropriate entities in a timely manner. Verify that garnishments comply with legal limits.

-

Comprehensive Document Gathering and Organization:

- Payroll Registers: Have detailed payroll registers readily available, showing gross pay, deductions, net pay, and cumulative totals for each employee and pay period.

- Timesheets/Timekeeping Records: Maintain clear, approved records for all hours worked, especially for non-exempt employees.

- Pay Stubs: Keep copies of pay stubs or ensure they are accessible through an employee portal, detailing earnings and deductions.

- W-2s and 1099s: Have copies of all W-2s (for employees) and 1099s (for independent contractors) issued for the audit period.

- W-4s (Employee Withholding Certificates): Verify that current W-4 forms are on file for all employees, ensuring correct tax withholdings.

- Forms 941/940 and State Tax Returns: Ensure all federal payroll tax returns (Form 941 for quarterly reporting, Form 940 for annual FUTA) and corresponding state unemployment and withholding tax returns are accurately filed and paid.

- General Ledger Payroll Accounts: Reconcile payroll-related general ledger accounts (wages expense, payroll tax expense, various liability accounts) to ensure they match payroll reports.

- Bank Statements and Reconciliations: Provide bank statements showing payroll disbursements and related reconciliations to verify payments.

- PTO/Leave Records: Maintain accurate records of paid time off accruals, usage, and balances.

- Benefit Documentation: Keep records of benefit plans, enrollment forms, and premium payments (e.g., health insurance, retirement plans).

- Garnishment/Child Support Orders: Have copies of all legal orders for wage garnishments or child support deductions.

-

Thorough Reconciliation and Verification:

- Payroll to Bank Reconciliation: Reconcile total payroll disbursements to bank statements to confirm all payments cleared correctly.

- Payroll to General Ledger Reconciliation: Ensure the total wages and payroll tax expenses in the payroll system match the general ledger.

- Quarterly/Annual Reconciliation: Reconcile quarterly Form 941 filings to the annual W-2s and Form 940 to ensure consistency.

- Deduction Reconciliation: Verify that amounts withheld for benefits, 401k, etc., are accurately remitted to the respective providers.

-

Review of Policies and Procedures:

- Payroll Policy Manual: Have a current payroll policy manual that outlines procedures for timekeeping, approvals, pay rates, deductions, and termination processes.

- Compensation Structure: Review compensation policies, bonus structures, and commission agreements to ensure they are consistently applied and properly documented.

- Internal Controls: Assess the effectiveness of internal controls related to payroll, such as segregation of duties (e.g., different people for time approval, payroll processing, and bank reconciliation).

-

Proactive Internal Checks:

- Spot Checks: Regularly perform internal spot checks on a sample of payroll entries to catch errors before an official audit.

- Employee Feedback: Encourage employees to review their pay stubs and report any discrepancies promptly.

-

Addressing Common Pitfalls Before External Review:

- Incomplete Documentation: Missing timesheets, unapproved expense reports, or absent W-4 forms are frequent issues. Ensure all documents are complete and signed.

- Inaccurate Classification: Misclassifying employees as independent contractors or miscategorizing exempt vs. non-exempt status can lead to significant penalties.

- Incorrect Overtime Calculations: Failing to properly calculate overtime pay, especially for complex situations involving bonuses or commissions.

- Unreconciled Accounts: Discrepancies between payroll reports, bank statements, and the general ledger.

- Late Tax Deposits: Penalties accrue quickly for late or incorrect payroll tax deposits.

- Outdated Employee Data: Incorrect addresses, withholding elections, or expired benefit enrollments.

- Lack of Segregation of Duties: Allowing one person to handle all aspects of payroll increases fraud risk.

Technological Facilitation: The Role of Payroll Software for Audit Preparation

In the modern business environment, robust payroll and accounting software is not just a convenience; it’s a strategic asset for audit preparation and compliance. Solutions like Patriot’s accounting and payroll software are designed to streamline audit readiness by automating many of the tasks that traditionally make audits burdensome:

- Centralized Data Management: The software provides a single, secure repository for all payroll and financial data, making it easy to retrieve documents, reports, and transaction histories.

- Automated Calculations: Eliminates manual calculation errors for wages, taxes, and deductions, ensuring accuracy from the outset.

- Real-time Reporting: Generates comprehensive payroll registers, tax reports, and general ledger reports on demand, significantly reducing the time spent compiling data for auditors.

- Tax Compliance Management: Automatically calculates, files, and deposits federal, state, and local payroll taxes, minimizing the risk of penalties for late or incorrect payments.

- Audit Trails: Maintains detailed audit trails for every transaction and change, providing a clear history of activities for verification purposes.

- Secure Employee Portals: Allows employees to access their pay stubs and W-2s securely, reducing administrative burden and ensuring data availability.

- Integration with Accounting: Seamlessly integrates payroll data with the general ledger, simplifying reconciliation and ensuring financial statements are consistent.

- Data Security: Protects sensitive payroll information with robust security measures, reducing the risk of data breaches.

Broader Implications and Future Outlook

The landscape of auditing is continually evolving, driven by technological advancements and increasingly complex regulatory environments. The emergence of big data analytics, artificial intelligence (AI), and blockchain technology is poised to transform auditing practices further, moving towards more continuous, real-time monitoring and predictive analytics. This shift implies that businesses, particularly those leveraging advanced software, will have even greater capabilities for proactive risk management and audit readiness.

Ultimately, integrating regular, strategic audits into a company’s operational rhythm is a hallmark of a well-managed and forward-thinking organization. It’s about moving beyond mere compliance to foster a culture of accuracy, transparency, and continuous improvement. By embracing audits as a tool for internal growth and resilience, businesses can not only navigate potential external scrutiny with confidence but also unlock greater efficiency, mitigate risks, and build a stronger foundation for sustainable success.

Frequently Asked Questions (FAQ)

- What documents do I need for a payroll audit? Key documents include payroll registers, timesheets, pay stubs, W-2/1099s, W-4s, Forms 941/940, state tax returns, general ledger payroll accounts, bank statements/reconciliations, PTO records, and detailed benefit/garnishment documentation.

- How often should payroll audits be conducted? Light internal checks are advisable quarterly or semi-annually, with a comprehensive annual review being a best practice. Increase frequency if significant errors have occurred, or during periods of rapid growth or significant changes in regulations.

- Who should conduct an internal audit? An internal audit should ideally be conducted by a knowledgeable internal team member who is independent of the day-to-day processing of the audited area to maintain objectivity. For added assurance, or for areas requiring specialized expertise, an external accountant or consultant can be engaged.

- What’s the difference between an internal audit and an external (financial) audit? Internal audits are conducted by employees for management’s benefit, focusing on improving internal controls, risk management, and operational efficiency. External audits are performed by independent third parties to provide an objective opinion on the fairness of financial statements for external stakeholders.

- How long does an internal audit take? The duration varies significantly based on scope and company size. A small, focused audit might take a few days, while a company-wide audit could extend for several weeks. Strong organization, robust internal controls, and the use of modern software can significantly reduce the time required.

- Can audits prevent IRS audits? No audit can entirely "prevent" an IRS audit, as these can be random or triggered by various factors. However, regular internal reviews drastically reduce the risk of an IRS audit by improving the accuracy and compliance of financial records and tax filings, making a business less likely to raise red flags.

Looking for accounting software that makes it easy to keep records without consuming all your valuable time? Try Patriot’s online accounting! We created our software with the input of business owners and accountants to make managing your books fast, easy, and affordable. Get your free trial today!

This article has been updated from its original publication date of September 15, 2022.

This is not intended as legal advice; for more information, please click here.

{kind=link}