The Evolution of Digital Payments: How Buy Now Pay Later is Transforming the E-Commerce Landscape for WooCommerce Merchants

The global e-commerce sector is currently witnessing a fundamental shift in consumer behavior, driven by the rapid adoption of Buy Now, Pay Later (BNPL) services. As digital storefronts evolve, the checkout experience has become the primary battleground for customer retention and conversion. For merchants operating on the WooCommerce platform, the integration of flexible payment solutions like Affirm, Afterpay, and Klarna is no longer merely an optional feature but a strategic necessity. By allowing shoppers to divide significant purchases into manageable, often interest-free installments, BNPL providers are effectively lowering the barrier to entry for high-value goods while ensuring that merchants receive full payment upfront. This financial model transfers the risk of credit and fraud from the small business owner to the multi-billion-dollar lending institution, creating a stabilized environment for growth in an increasingly volatile economic climate.

The rise of BNPL can be traced back to the early 2000s, with the founding of Klarna in Sweden in 2005, followed by Affirm in 2012 and Afterpay in 2014. However, the true explosion of the service occurred during the COVID-19 pandemic, as brick-and-mortar limitations pushed consumers toward online shopping. During this period, consumers became more cautious about traditional revolving credit card debt, seeking instead the transparency of fixed-payment schedules. Today, the BNPL market is projected to reach a valuation of several trillion dollars globally by the end of the decade, reflecting a permanent change in how the modern shopper manages their personal cash flow.

The Mechanics of Modern Installment Lending

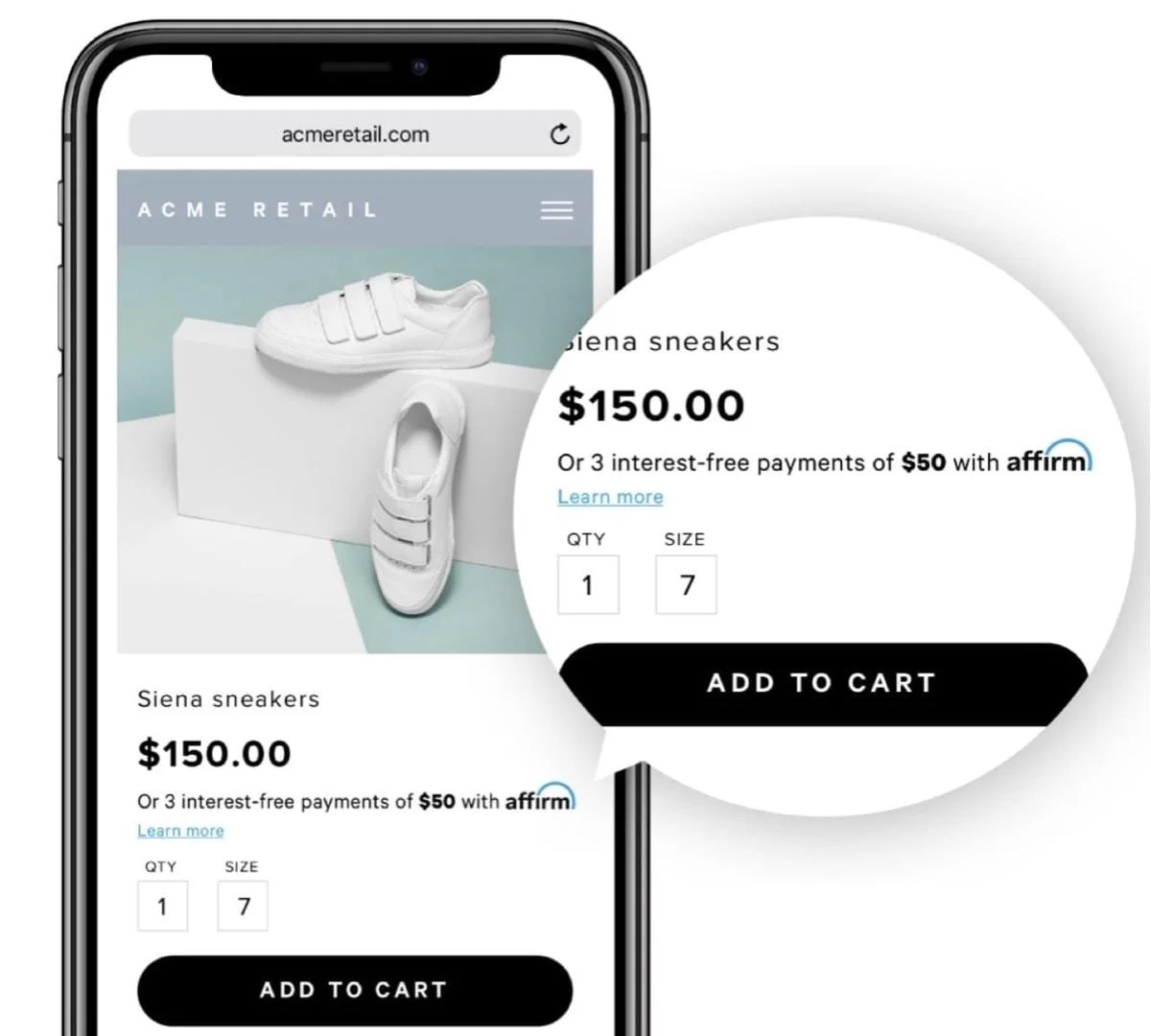

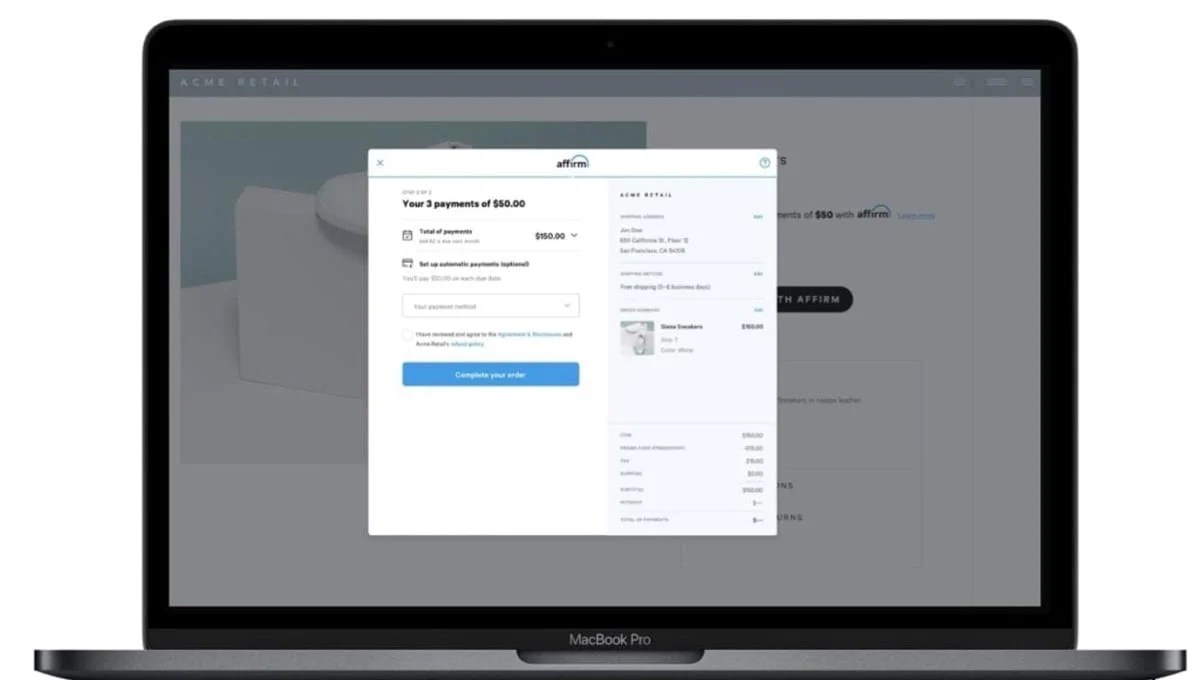

At its core, BNPL is a modernized version of the traditional "layaway" plan, with one significant difference: the customer receives the product immediately. When a shopper selects a BNPL option at a WooCommerce checkout, the provider performs a real-time, usually "soft" credit check that does not impact the customer’s credit score. Upon approval, the provider pays the merchant the full purchase price of the order, minus a small transaction fee. The customer then pays the provider back in a series of installments—typically four payments over six weeks or longer-term monthly financing for larger items.

This arrangement offers a dual layer of protection. For the consumer, it provides an alternative to high-interest credit cards. For the merchant, it eliminates the administrative nightmare of managing payment plans internally. Historically, merchants who attempted to offer their own financing faced significant overhead, including the need to chase late payments, manage expiring credit cards, and handle complex refund calculations. By outsourcing these tasks to dedicated providers, store owners can focus on product development and marketing while the BNPL firm handles underwriting, collections, and dispute management.

Data-Driven Benefits for E-Commerce Merchants

The adoption of BNPL is supported by compelling empirical data that points toward a direct correlation between flexible payments and increased revenue. According to industry reports from Afterpay, retailers utilizing their platform see an average 22% increase in cart conversions. This suggests that a significant portion of "window shoppers" who would otherwise abandon their carts due to price friction are converted into buyers when presented with the option to pay in smaller increments.

Furthermore, the impact on Average Order Value (AOV) is substantial. When the psychological barrier of a large lump-sum payment is removed, customers are more likely to add additional items to their cart or opt for higher-tier versions of a product. Studies indicate that Afterpay retailers experience an average 40% increase in order value. This phenomenon is particularly evident in the "Pay-in-4" model, where a $200 purchase is framed as four payments of $50. By breaking down the cost, the merchant protects their profit margins, reducing the need for aggressive discounting to move inventory.

The demographic shift is equally important. Gen Z and Millennial shoppers, who are increasingly wary of traditional banking institutions, represent the largest user base for BNPL services. Approximately 73% of Afterpay’s 20 million global customers belong to these younger generations. For a WooCommerce merchant, offering BNPL is a direct signal of brand modernism and customer-centricity, qualities that foster long-term loyalty among digital-native consumers.

A Comparative Analysis of the "Big Three" Providers

Choosing the right BNPL partner requires an understanding of the specific strengths and regional reaches of the major players in the market. While Affirm, Afterpay, and Klarna all offer installment payments, their models differ in ways that can impact a merchant’s specific business goals.

Affirm: The Specialist for High-Value Transactions

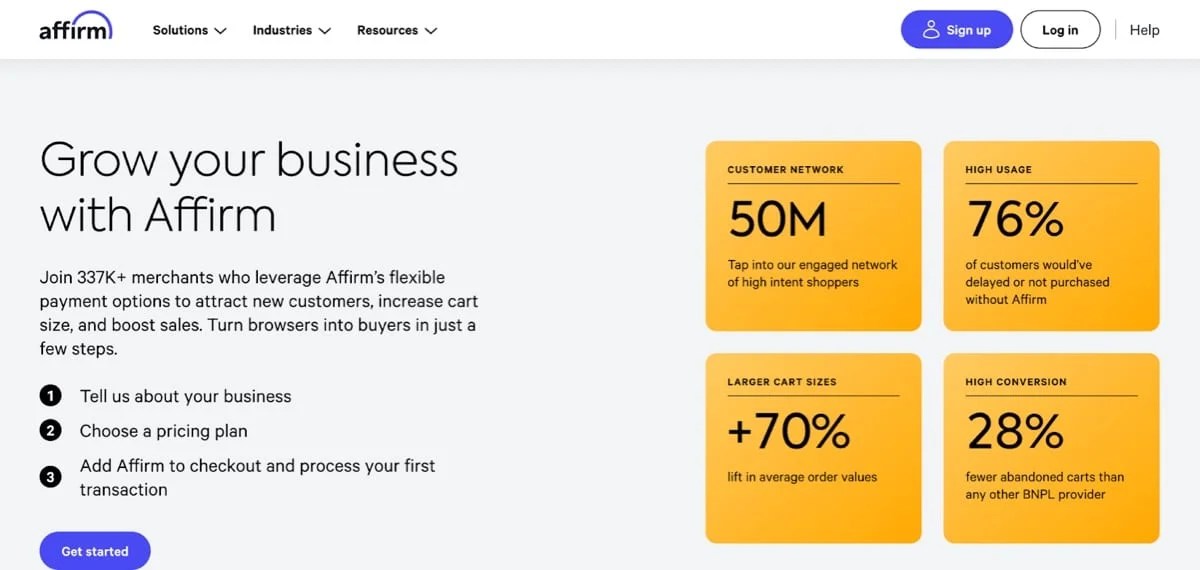

Affirm has positioned itself as the premier choice for merchants selling premium or luxury goods. With the ability to finance carts ranging from $35 up to $30,000, Affirm offers flexible terms that can extend up to 36 months. This makes it ideal for industries such as home furniture, high-end electronics, and fitness equipment. Affirm’s commitment to transparency—promising no late fees or hidden costs—builds a high level of trust with consumers planning major life purchases.

Afterpay: The Retail and Fashion Powerhouse

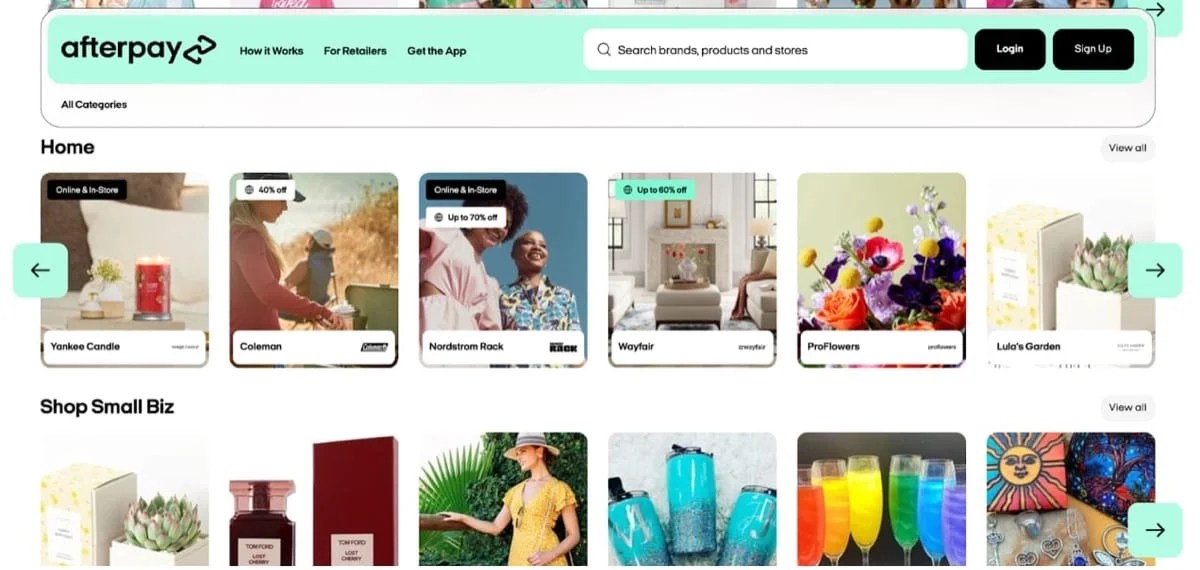

Afterpay, now part of the Block (formerly Square) ecosystem, is renowned for its "Pay-in-4" model and its massive directory of retail partners. It excels in the fashion, beauty, and lifestyle sectors where AOV typically stays under $3,000. One of Afterpay’s greatest strengths for WooCommerce merchants is its ability to drive new traffic; nearly 30% of Afterpay shoppers are reportedly new to the brands they discover through the Afterpay app directory.

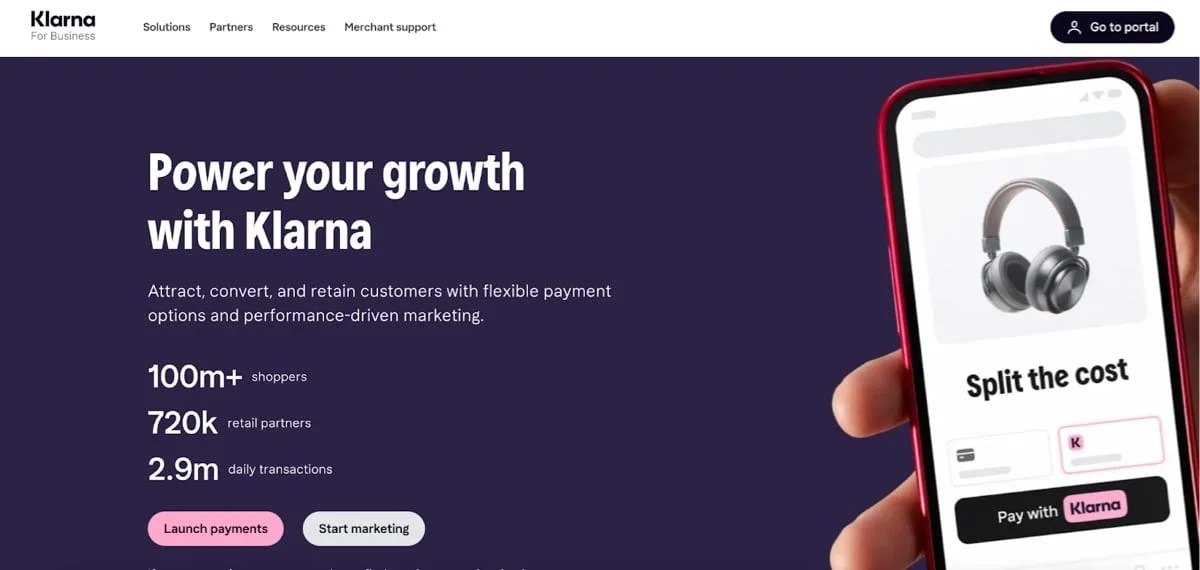

Klarna: The Global All-in-One Solution

With a presence in 26 global markets and over 150 million active users, Klarna offers the most comprehensive international reach. It provides a variety of payment methods, including "Pay in 30 days," "Financing," and "Pay in Full." Klarna’s infrastructure is designed to be a total commerce network, offering merchants performance-based media tools to place their products in front of high-intent shoppers across multiple digital channels.

Integration Strategies for WooCommerce

WooCommerce offers several streamlined pathways for merchants to activate these services, ensuring that the technical barrier to entry is low.

- WooPayments Integration: For many merchants, the most efficient method is through WooPayments. This native solution allows store owners to manage BNPL transactions alongside traditional credit card payments from a single, unified dashboard. This eliminates the need for multiple extensions and provides a centralized view of all financial data, which is critical for accurate bookkeeping and cash flow forecasting.

- Stripe Integration: Merchants already utilizing Stripe for their payment processing can often activate BNPL options directly through their existing Stripe settings. This allows for a quick rollout of Affirm, Afterpay, or Klarna without significant changes to the site’s underlying architecture.

- Standalone Extensions: For businesses that require more granular control or specific features offered by a single provider, standalone extensions are available on the WooCommerce Marketplace. These extensions often include specialized marketing assets, such as "price-on-installment" messaging that appears on product pages, which has been shown to improve click-through rates.

Mitigating Risk and Ensuring Compliance

A common concern among merchants is the potential for fraud or non-payment. However, one of the most attractive features of the BNPL model is that the provider assumes nearly all the risk. When a transaction is approved, the merchant is guaranteed payment. If a customer fails to meet their installment obligations, the BNPL provider manages the loss. Furthermore, in the event of fraud-related disputes or chargebacks, the lenders typically take on the associated costs and investigative labor.

From a regulatory perspective, the BNPL industry is coming under increased scrutiny from organizations like the Consumer Financial Protection Bureau (CFPB). While this may lead to stricter underwriting standards in the future, it also lends a layer of legitimacy and stability to the sector. Merchants are encouraged to stay informed about these changes, though the primary burden of compliance rests with the BNPL providers themselves.

Broader Economic Implications and Future Outlook

The integration of BNPL into the WooCommerce ecosystem is part of a broader trend toward the "democratization of credit." By providing interest-free alternatives to traditional banking, these services are allowing a wider range of consumers to participate in the digital economy. For the merchant, this means a larger total addressable market and the ability to maintain sales volume even during periods of economic contraction.

As we look toward the future, the distinction between online and offline payments will continue to blur. Many BNPL providers are now offering physical cards or digital wallet integrations that allow consumers to use installment plans at in-person points of sale. For WooCommerce merchants with omnichannel aspirations, establishing a relationship with a BNPL provider now creates a foundation for future growth across all sales platforms.

In conclusion, Buy Now, Pay Later is more than a checkout trend; it is a fundamental reconfiguration of the merchant-consumer relationship. By prioritizing flexibility, transparency, and risk mitigation, BNPL services empower WooCommerce store owners to scale their businesses with confidence. Whether through increased conversion rates, higher average order values, or access to a younger, more dynamic demographic, the benefits of BNPL are clear. As the e-commerce landscape continues to grow more competitive, the ability to meet customers where they are—financially and technologically—will remain the hallmark of successful digital entrepreneurship.

{kind=link}